{kind=link}

Source: Credit Link

In the last 11 years, more than 600,000 people in the United States borrowed roughly $1.05 billion from American Web Loan, an online payday lending service that promises fast and convenient loans to people in dire financial circumstances. The company’s website features video testimonials from customers who say that in the face of medical bills or car repairs, American Web Loan quickly gave them the cash advance they needed to handle unexpected emergencies.

What the testimonials leave out is the exorbitant interest rates American Web Loan charges its borrowers. According to documents from a federal class-action lawsuit filed against the company in late 2017, American Web Loan’s average interest rate for its $300 to $2,500 offerings was more than 560 percent. Almost two-thirds of customers have managed to pay back their loan — plus around $472 million in interest — but many have been unable to shoulder the additional debt.

In 15 states the interest rates charged by American Web Loan were illegal; in others where payday lenders can register with the state to seek exemptions, the company never has. American Web Loan claimed it could charge sky-high rates because it was owned by a Native tribe, the Otoe-Missouria. The tribe’s sovereign status meant that the business would have immunity against state usury laws and civil suits. However, a judge ruled that American Web Loan had no claims to tribal sovereignty because it actually belonged to the tribe’s business partner, Mark Curry, who’s made a career out of predatory lending.

“If anything, he’s controlling the tribe. The tribe isn’t controlling him. And he’s continuing to do that,” Judge Henry Coke Morgan Jr. said to American Web Loan’s attorney during a 2019 hearing. “The tribe’s being, in effect, paid a royalty for your client to wear – what is it they call it? – the ermine cloak of sovereign immunity? That’s all it is.”

The case, which reached a preliminary settlement agreement in April, generated extensive discovery about American Web Loan’s business dealings over the last decade and provides an unprecedented look under the hood of a major “rent-a-tribe” operation, a once-popular financial services model among payday lenders and their Wall Street and Silicon Valley investors. (Lawyers for Curry and American Web Loan declined to comment on the record; the preliminary settlement agreement prohibits all involved parties from speaking to the press.)

In 2009, Curry approached the chair of the Otoe-Missouria, John Shotton, to set up an online lending company under the tribe’s jurisdiction. Behind the scenes, court records reveal that Curry and his labyrinth of companies handled almost every aspect of American Web Loan’s operation. As loan repayments began and the company became flush, Curry reaped millions in profits and began seeking out investors to grow the business.

Amid federal and state crackdowns on “rent-a-tribe” operations starting in 2013, Curry eventually arranged with Shotton to sell the companies that ran American Web Loan to the Otoe-Missouria. The $200 million deal allowed Curry to continue running the business in the background and saddled the tribe with insurmountable debt — just like what happened to many of American Web Loan’s customers.

“Tribes have to make money, but doing it at the expense of the public gives tribal sovereignty a bad name,” said Nathalie Martin, a University of New Mexico law professor who has written about alliances between payday lenders and Native tribes. “When you use your sovereignty for these types of things, it could be seen as weakening and cheapening that sovereignty.”

Setting Up Shop

By the time he met the Otoe-Missouria leadership, Curry had already made a name for himself in the payday lending industry. The 53-year-old native of the Kansas City area — home of online payday lenders — specialized in “rent-a-bank” arrangements, in which lenders made pacts with federal banks based in states with no interest rate caps to shield themselves from state lending laws. His companies, Geneva Roth Ventures and Geneva Roth Capital, had partnered with banks in Utah to loan money to borrowers nationwide through the website Loan Point USA. But as regulators banned or fined Curry’s “rent-a-bank” operation in at least seven states, he began searching for a new venture.

What he came up with appeared in a presentation to potential investors in American Web Loan: the sovereign nation model.

-

Mark Curry set up American Web Loan as a tribal corporation in 2010 with the Otoe-Missouria Tribe. However, Curry’s companies controlled almost every aspect of business operations.

-

Curry made millions in profits and sought to expand the business around the same time that state and federal regulators began cracking down on “rent-a-tribe” lenders.

-

In 2016, Curry and Otoe-Missouria Chair John Shotton arranged for the tribe to buy the companies behind American Web Loan, putting the tribe $200 million in debt — to Curry.

-

The judge in a class-action lawsuit ruled that American Web Loan is not a tribal business because Curry did not actually hand over ownership to the tribe and still controlled the company. The case reached a preliminary settlement agreement in April.

Shotton, then the 32-year-old chair of the Otoe-Missouria Tribe, saw in American Web Loan a new revenue source. About 40 percent of the Otoe-Missouria, a tribe of roughly 3,000 members based in tiny Red Rock, Oklahoma, lived below the federal poverty line. At the time, four casinos had been the tribe’s economic engine; its members received quarterly payments of around $700 from gaming, according to the tribe’s newsletters. But that revenue had come under threat from new establishments across the border in Kansas.

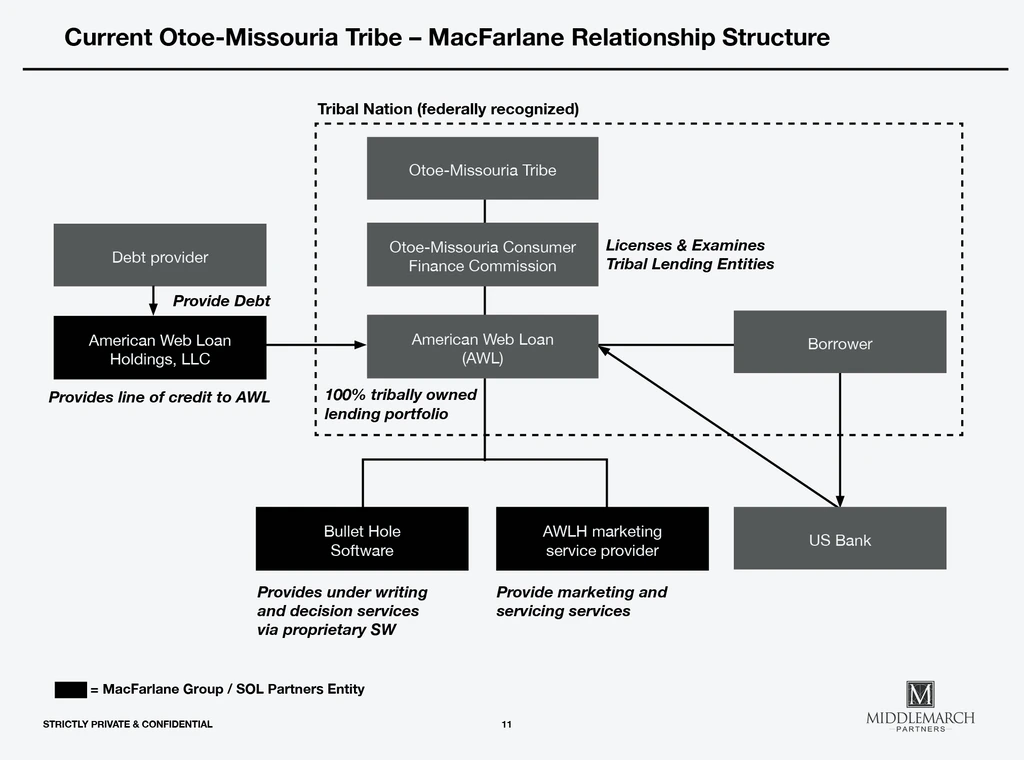

Curry and the tribe’s leaders went into business, a relationship that was first reported by Bloomberg News. The Otoe-Missouria council created American Web Loan as a tribal corporation, but it was the lender in name only. Despite Curry’s claim that he was just a consultant for the company, slides from the investor presentation attached as exhibits in court filings show him as CEO of all the companies behind it, with “100% Ownership or Control.” MacFarlane Group, his successor to Geneva Roth, ran the lending operation, and he signed a service agreement with American Web Loan, he would later testify, that his companies would handle practically every aspect of business operations: lead generation, follow-up communications, loan processing, money transfers, software management, customer support, credit reporting, and collections.

The tribe’s contributions were largely cosmetic: It appointed a nominal head to write out the loan checks, according to the tribe’s then-vice chair, and set up a call center in Red Rock and a consumer finance regulatory body whose ordinances would create the impression of oversight. Only six out of 50 American Web Loan employees were from the tribe, and they all worked in the Red Rock call center. (Shotton later testified that the company had hired an additional four tribal members.)

American Web Loan told borrowers that their loans were governed by tribal law — not federal law or the laws of their home state. They had to enroll in automated bank transfers to get the money; the first repayments would often be automatically deducted from the registered account two weeks later. Ironically the Otoe-Missouria’s own members could not borrow from the tribe’s lender — charging members such astronomical interest rates is illegal under the tribal criminal code.

“The way we look at it at the tribal level is we developed our own code, developed the rules around lending,” Shotton said when asked about American Web Loan’s interest rates in court in 2019. “We’re very protective in a fair way. We have great consumer protection.” (Tribal council leaders and other members did not comment for this story.)

Curry’s companies carried the ultimate financial risk and reward: His company American Web Loan Holdings LLC purchased a loan from the lender at a small premium about two weeks after it was established. The company kept 99 percent of the loan portfolio, while the tribe retained 1 percent — a fair split, according to Curry, since both sides had agreed. From February 2010 until September 2016, Curry testified that his firm’s share of the profits amounted to around $110 million. In comparison, the tribe only received about $8 million.

Expanding the Empire

In 2011, American Web Loan’s first full year in operation, the amount of loans the company disbursed rose 71 percent, from $35 million to $59.7 million, according to the class-action complaint. Over the next three years, Curry sought financing of at least $110 million from private equity firms, hedge funds, and other investors. He made the pitches with the help of at least two investment banking firms including Middlemarch Partners, which is named in the 2017 lawsuit for its role in helping finance the allegedly illegal operation. Curry’s MacFarlane Group spent $15 million annually on marketing, which, according to a 2013 Middlemarch presentation to potential investors filed as an exhibit in the complaint, made it and its clients “among the largest acquirers of leads in online consumer lending.”

An early investor was a $470 million hedge fund called Medley Opportunity Fund II LP, which provided American Web Loan Holdings with a loan of almost $23 million in late 2011. Brothers Brook and Seth Taube, who ran the fund and were also named in the lawsuit, were familiar with the payday lending industry, previously investing in a payday store chain. (Lawyers for Medley and Middlemarch did not return requests for comment.)

The Taubes were not passive investors. As part of their credit agreement with American Web Loan Holdings, Medley required monthly, quarterly, and annual financial statements, plus weekly reports “providing in reasonable detail fees earned and default percentages on loan portfolios.” Curry also had to furnish the documents he had signed with the tribe’s leadership to establish American Web Loan; if they were ever changed without Medley’s consent, the fund could terminate the loan it had made to Curry’s American Web Loan Holdings.

American Web Loan became one of Medley’s top performers. But in at least one of Medley’s investor presentations, it was referred to only as “Online Consumer Finance Platform” while Medley’s 15 other investments were named. Because its identity was hidden, Medley’s investors, some of which were public employee pension plans, would not see that a payday lender was in the fund’s portfolio. Of all the companies listed, American Web Loan boasted the highest cash yield (15 percent) and gross contractual return (25.6 percent).

American Web Loan had emerged as a massive and complex lending enterprise: American Web Loan Holdings was the borrower, and another 30 companies — all of them fully or partially owned by Curry — appeared in its corporate structure and provided different lending functions, according to Medley’s credit agreement. All but two had the same primary place of business: a nondescript single-story office building outside Kansas City. Companies like “Dinero” and “Chieftain” were listed as holding loan portfolios; based on other presentations, as well as their curious names, these entities might have been intended to mask the identities of investors outside of Curry’s web of businesses, according to the complaint, since the Medley loan only accounted for part of the venture capital Curry was seeking.

With Medley’s backing, Curry luxuriated in American Web Loan’s explosive growth. According to real estate records, he purchased a $1.8 million mansion in the Las Vegas suburbs. In late 2012, he moved to Puerto Rico, where he created SOL Partners, a firm that provided Spanish-language call center services to the payday lending industry, and a private family foundation that supports programs for Native causes and cultural preservation, according to its website.

By 2013, SOL Partners joined MacFarlane Group to manage the key lending functions of American Web Loan and provide capital, according to the Middlemarch presentation. Despite the Otoe-Missouria’s limited role in American Web Loan, in the presentation the tribe appears in the middle of Curry’s lending empire — a linchpin onto which Curry would later fasten his entire legal defense.

Crackdown on Tribal Lenders

The Otoe-Missouria is among dozens of tribes that entered into dubious arrangements with online payday lenders beginning in the mid-2000s. Elsewhere in Oklahoma, for instance, the Modoc Tribe and the Miami Nation partnered with Scott Tucker, a former race car driver and payday lender who later became a subject of the Netflix series “Dirty Money.” Together with his attorney, Timothy Muir, and the Santee Sioux of Nebraska, they created a multibillion-dollar payday operation in which the tribes appeared to be in control. Many tribes created multiple lending websites; the Otoe-Missouria Tribe also established two other lending companies — Great Plains Lending and Clear Creek Lending — that targeted different customer bases than that of American Web Loan.

It wasn’t long before federal and state regulators started looking into tribal lenders. In early 2013, the Justice Department began investigating online payday lenders and the third-party payment processors that handled their bank transactions. In August, the New York State Department of Financial Services sent cease-and-desist letters to 35 online lenders, 11 of which were purportedly tribal-owned or affiliated — including American Web Loan and Great Plains Lending. The department also sent letters to 117 state and nationally chartered banks as well as Nacha, the administrator of the automated clearing house network through which electronic financial transactions are processed, asking for help in “choking off” the online money transfers that the lenders depended on.

It wasn’t long before federal and state regulators started looking into tribal lenders.

The Otoe-Missouria, along with the Lac Vieux Desert Band of Lake Superior Chippewa Indians based in Michigan, sued for an injunction against that state department in New York federal court. According to courtroom testimony, the tribes’ legal fees were paid from the membership dues of the Native American Financial Services Association, an industry lobbying group Curry helped create.

The lawsuit became one of the first tests of the legal framework behind “rent-a-tribe” operations. In their complaint, the tribes invoked their sovereign immunity and challenged the department’s authority to impose state laws on tribal businesses.

In response, New York’s attorney general wrote that his state’s usury statutes indeed applied to financial transactions between tribes and New York consumers “when those transactions have significant and injurious off-reservation effects — as is the case here, given the crippling debt that payday loans cause to New Yorkers.”

The Southern District of New York ruled against the tribes. On appeal, the Second Circuit upheld the decision, concluding that the tribes hadn’t provided sufficient evidence to prove that their internet loans should count as on-reservation activity.

The Otoe-Missouria’s troubles only escalated from there. In a one-year period beginning in February 2013, the Federal Trade Commission received 461 complaints against American Web Loan and Great Plains Lending — second only to lenders affiliated with the Miami Tribe.

In early 2015, Connecticut’s Department of Banking fined Shotton $700,000 and Great Plains Lending and Clear Creek Lending a combined $800,000 for making loans to Connecticut residents that violated the state’s interest rate cap. Shotton filed a federal civil rights lawsuit in Oklahoma against Connecticut regulators, but the rulings were upheld in Connecticut two years later.

Up until then, the masterminds behind the tribal lenders had largely avoided legal scrutiny. This changed in 2016, when Tucker and Muir were arrested on federal racketeering charges tied to their $3.5 billion “rent-a-tribe” operation. Prosecutors described their ownership arrangements with the three tribes — the Miami, Modoc, and Santee Sioux — as shams.

Tucker and Muir were convicted and sentenced to nearly 17 years and seven years in prison, respectively, sending shockwaves through the online payday industry. The tribes accepted non-prosecution agreements, admitted in court to overstating their roles to help Tucker and Muir elude state laws, and forfeited their proceeds: $48 million from the Miami and $3 million between the Modoc and Santee Sioux. The tribes’ cuts of the profits were reportedly 1 percent of the revenues — the same as the Otoe-Missouria.

It was around the time of the arrests that Curry began talking to Shotton about selling the tribe the companies behind American Web Loan.

“The Tribe Owns the Business”

Despite the state legal battles and mounting consumer complaints, American Web Loan’s business hadn’t suffered. From 2013 until September 2016, American Web Loan Holdings brought in revenues of almost $670 million, and Curry himself was receiving an average of $18 million a year, according to courtroom testimony. Shotton claimed in his 2019 testimony that the company was valued at $340 million.

Curry’s name never appeared on court documents in the New York case, and Shotton wrote in his sworn declaration that the Otoe-Missouria wholly owned and operated its lending companies. As the walls appeared to be closing in on tribal lenders, Curry and Shotton agreed that the tribe would buy American Web Loan’s infrastructure for $200 million — an amount the tribe did not have.

According to court records, Curry sold MacFarlane Group to the tribe through seller take-back financing: Companies owned by Curry would loan about half the $200 million to the tribe, and the tribe would pay the rest over a five-year consulting deal with Curry’s SOL Partners that it wouldn’t be able to get out of regardless of SOL’s performance. This arrangement allowed Curry to pay less taxes on the sale, he later testified, and the tribe to make fewer interest payments.

The tribe now had to pay about $4 million to Curry every month for the next five years.

On September 8, 2016, the Otoe-Missouria formed a new entity called Red Stone to purchase MacFarlane, American Web Loan Holdings, and Bullet Hole, Curry’s software company. According to court records, Red Stone borrowed about $95 million, plus 10 percent interest, from three of Curry’s new companies, all of which were created a week later. The remaining balance of roughly $100 million would be paid through SOL Partners. The management team continued to operate out of the same corporate offices; the tribe had to pay Curry rent for the MacFarlane Group office he owned in Las Vegas.

The Otoe-Missouria council approved the deal in a special session on September 21, 2016, with five in favor, one abstaining, and one absent. The tribe now had to pay about $4 million to Curry every month for the next five years.

Curry and Shotton denied in court that the acquisition was meant to give the appearance of ownership to the tribe and shield Curry from liability. After six years in business, Shotton claimed that the tribe had been ready to buy MacFarlane Group, to which he said it had “outsourced” certain operations.

Shotton spoke about the unusual financing structure in a 2018 deposition: “The tribe didn’t care. The tribe wants the business in five years. They want to be in control of everything.” Yet in court the following year, he insisted that “the tribe owned and operated the business from day one.”

In an email Curry sent to Shotton in July 2016, he wrote, “It was more clear that the tribe owns the business and not me.” Curry also noted that the tribe still “gets the same as what was originally contemplated. The tribe will have everything they need to run the business.”

American Web Loan 2.0

The “new” American Web Loan chose not to do business in states where regulators had challenged its practices, including Connecticut and New York. According to court documents, the tribe’s cut would come out of a pool of money that also paid for operating expenses and the monthly loan repayments to lenders owned by Curry. The tribe would receive 3.6 percent of the revenues, up from 1 percent. Shotton and the tribal council decided to put half of the profits in the tribe’s general fund and the other half in its economic development authority to help fund its cattle-ranching company and a new propane business. The tribe’s first draw in 2017 was $6 million, an amount that was scheduled to increase by $1 million annually until the loan was paid off.

About a month after the deal was approved, Curry’s chief marketing officer sent him an email, dated November 3, 2016, about how the tribe’s debt posed “challenges” to revenue generation, according to courtroom testimony.

“We’re in a bit of a catch-22,” the email read. “AWL must generate specific EBITDA to support and fund the note” — referring to earnings before interest, taxes, depreciation, and amortization, or the company’s profitability. “On paper, it seems obvious that we need to push rates higher to drive EBITDA; however, consumer demand for higher rates is uncertain.”

After the merger, American Web Loan raised its interest rates beyond 700 percent. According to the class-action complaint, direct-mail solicitations were made to look like a check payable to the recipient, enticing them to follow up on their “pre-approval” for a loan: “Get $1,500 in as little as 1 day!” Some borrowers claimed that they had not been told the rate or the total payment they would owe, saying they got a copy of their loan agreement only after receiving the money.

Curry denied in court that the company’s skyrocketing interest rates were connected to the Otoe-Missouria’s debt to him. “I believe there was a shifting of the credit bands that we used,” he said. “I don’t believe that it was a wholesale shift up.”

The new Trump administration soon calmed the alarm over Tucker and Muir’s case and began to pave the way for Curry to plot American Web Loan’s comeback. In mid-2017, the Justice Department ended its Obama-era investigation of online payday lenders. The following year, the Consumer Financial Protection Bureau dismissed a lawsuit against a group of tribal-affiliated lenders. “The federal became totally denuded in every single way,” said Martin, the law professor.

Curry set out to double or triple the size of American Web Loan’s loan portfolio in three to four years, according to the complaint. Middlemarch Partners, the firm that had previously helped him find investors, sent out a solicitation in 2017 seeking up to $90 million for Curry’s “top-five fintech company.” There was no mention of the sale to the Otoe-Missouria.

A Sword and a Shield

In 2018, Curry, American Web Loan, Middlemarch Partners, and Brook and Seth Taube of Medley Opportunity II Fund faced a class-action lawsuit for racketeering in Virginia federal court. By the time the preliminary settlement was reached last month, the class included 606,318 people who took out 1,055,376 loans from American Web Loan between January 1, 2012, and June 26, 2020, plus an unspecified number of individuals who borrowed money during the two years before that period when the company did not retain records.

Evidence in the case has shown that Curry did not actually hand over ownership of American Web Loan to the Otoe-Missouria but that he did appear to shift financial and legal risk from himself to the tribe.

Despite Shotton’s testimony that American Web Loan retained Curry as part of a “short-term transition,” Curry remained as CEO of the company four years after the loan deal and maintained control over day-to-day operations.

American Web Loan’s new board of directors — made up of Shotton, Curry, two of Curry’s associates, and two tribal members — met for the first time on November 8, 2016, in Oklahoma City, according to courtroom testimony. The board voted to appoint Curry as the head of the company and to pay each board member $5,000 per monthly meeting. They later raised it to $7,500. Seven months into the lawsuit, the board — which still included Curry — approved Curry’s request to pay his legal fees.

The board’s first meeting also included a request to the Otoe-Missouria council — on which Shotton and American Web Loan board member Ted Grant also served — to pass legislation to give Curry and the other non-Native board members tribal immunity, which was granted the following month.

In its loan agreements with Curry, the tribe had already waived its own sovereign immunity, and any change in tribal law or tribal government action against American Web Loan would lead to default. Curry claimed in court that he had no idea who wrote these provisions into the contracts.

In 2019, Morgan, the judge in the case, seized on the immunity request as evidence of Curry’s motive to retain control of the company and protect himself from liability — even if it came at the tribe’s expense. “He wants to use sovereign immunity as a sword and a shield,” Morgan said from the bench.

Curry did not actually hand over ownership of American Web Loan, but he did appear to shift financial and legal risk to the tribe.

Based upon well-established legal tests, Morgan ruled that American Web Loan was not a tribal business because Curry controlled virtually every part of its operation and that his and American Web Loan’s claims to immunity were invalid. As a result, the judge said the case could head to trial to take up the legality of the lending operation. The defendants claimed that tribal immunity applies to American Web Loan, Curry, and SOL Partners and that their lending activity was not subject to any state laws or regulations.

As for the Otoe-Missouria’s role, Morgan said, “The tribe benefits, up until now, in a very small way, but a very steep price is paid by the victims.”

Shotton and the other two board members from the tribe, all of whom were indemnified from the lawsuit, earned far more from the monthly board meetings than the Native company employees. Around the time the council granted Curry immunity, Shotton had asked him for a $25,000 bonus for himself and the other board members, according to courtroom testimony.

The parties in the lawsuit initially reached a settlement agreement more than a year ago, but after a handful of American Web Loan consumers objected in part to the inadequacy of its debt relief, Morgan rejected it in November. Per the terms of that original preliminary settlement, Curry resigned from the board and as CEO last June. In October, he signed an affidavit stating that the tribe’s loan payments to him would be suspended until the settlement went into effect, at which time the loan would end.

Morgan, who had ordered the parties back to mediation, gave temporary approval to a modified agreement last month. A final settlement hearing is scheduled for July 9.

The borrowers’ cash award will be $86 million, minus $18.5 million in attorneys’ fees — about a quarter of which will come from Curry and the rest from what American Web Loan would have given Curry as debt payments and consulting fees. Any outstanding debt the consumers owe to American Web Loan will be canceled, as well as close to $218 million worth of loans held by a trio of third-party debt buyers. Curry agreed to leave American Web Loan in all managerial and operational capacities on or before December 28, 2020.

American Web Loan is still in business, though it has agreed to change some of its practices. The company will modify its loan agreements to state that it will comply with applicable federal laws and to include the full cost of a loan. The company will also stop requiring borrowers to accept automatic bank withdrawals.

Without federal intervention, American Web Loan and other tribal payday lenders can continue exploiting borrowers’ financial needs to turn a profit. Right before last November’s election, the Treasury Department issued a rule change that would pave the way for the return of “rent-a-bank” operations that Curry made his name from.

“He went from doing the same thing with banks to applying the same theory to the Indian tribe,” Morgan said during a hearing. “He’s just in it to make the money.”

Source: Credit Link